✓ Meets Irish EEA director compliance requirements ✓ Revenue-approved non-resident director bond included ✓ Full documentation and CRO filing support ✓ Fast and hassle-free setup process ✓ Secure handling of all legal records ✓ Ongoing compliance and advisory support

This guide is written for contractors, freelancers, and independent professionals who are working or planning to work in Ireland and need a clear, honest understanding of how umbrella companies operate under the Irish PAYE system.

It is especially relevant if you are starting your first contract and do not know whether an umbrella company, a limited company, or a sole trader structure is the right fit. It is equally useful if your agency or client has told you that you must operate through PAYE and you want to understand exactly what that means for your take-home pay, your taxes, and your rights.

If you are new to Ireland, new to contracting, or simply tired of getting vague answers about how umbrella payroll actually works, this guide will give you the full picture in plain English, without the jargon.

In this guide, you’ll find:

A clear explanation of how an umbrella company works in Ireland and how you get paid through the PAYE system

A full breakdown of taxes, deductions, and typical costs involved including umbrella fees and what they actually cover

A practical, honest comparison between umbrella company, limited company, and sole trader structures and when each one makes sense

Step-by-step guidance on how to get started and what to expect throughout your contract

Key compliance points to ensure you stay fully aligned with Revenue requirements from day one

Key Takeaways

An umbrella company allows you to work as a contractor while being employed under PAYE removing the need to manage your own company, file tax returns, or handle payroll administration

It is the most suitable option when your agency or client requires a PAYE structure, or when your contract is short-term and the overhead of running a limited company is not justified

Your income is taxed at source through PAYE, PRSI, and USC meaning lower administration throughout the year, but less tax flexibility compared to a well-run limited company

Class A PRSI contributions give you access to the full range of Irish social welfare benefits including Jobseeker’s Benefit, Illness Benefit, and Maternity Benefit which is a meaningful advantage over self-employed and sole trader structures

A compliant umbrella provider should offer real-time payroll processing under Revenue’s PAYE Modernisation system, transparent and fixed fees, detailed payslips every pay period, and full adherence to all Revenue regulations if yours does not, that is a problem worth addressing before you sign anything

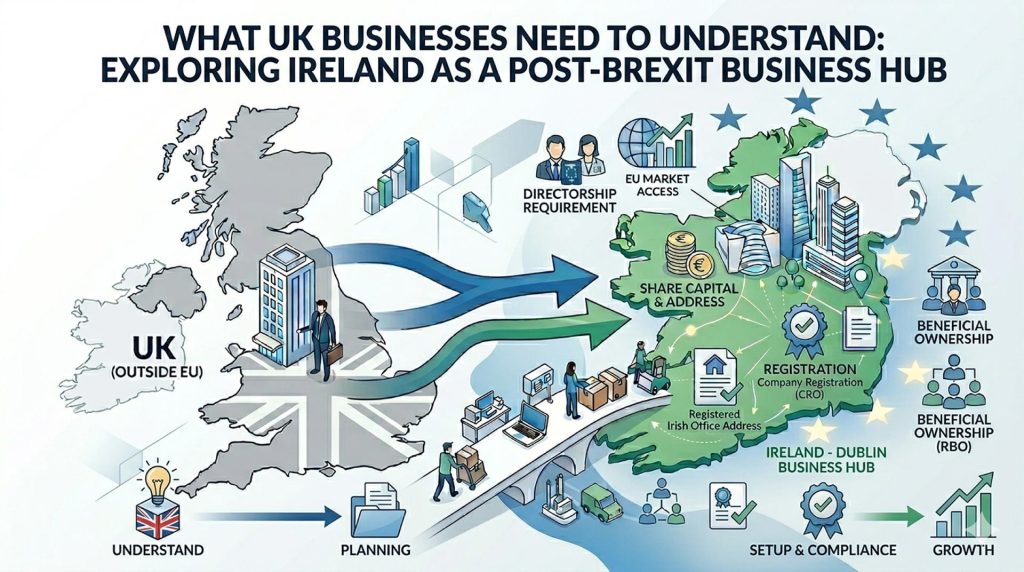

Why UK Businesses Are Still Looking at Ireland

Five years on from Brexit, the conversation has shifted. In the immediate aftermath of the UK leaving the EU, there was urgency, uncertainty, and a scramble to understand what the new rules actually meant in practice. That phase is over.

What remains is a steady, practical reality the UK is no longer inside the EU, and businesses that trade with, employ people in, or are regulated by EU member states face a permanent layer of additional complexity that did not exist before 2021.

For many UK businesses particularly those with significant EU revenue, EU-based clients, or EU regulatory obligations the most effective long-term response to that reality is not to navigate the friction, but to remove it. And the most practical way to do that is to form a company in Ireland.

This guide explains exactly why, and exactly how.

The Post-Brexit Business Landscape What Actually Changed

To understand why Irish company formation is such a compelling option for UK businesses, it helps to be clear about what Brexit actually changed from a commercial standpoint.

Customs and tariffs: Goods moving between the UK and EU are now subject to customs declarations and, in some categories, tariffs. This adds cost, complexity, and delay that did not previously exist.

VAT: Cross-border VAT rules between the UK and EU changed significantly. UK businesses selling goods to EU consumers now deal with import VAT, and the thresholds and procedures vary by member state.

Regulatory divergence: UK businesses operating in regulated sectors financial services, pharmaceuticals, medical devices, food production found that their UK regulatory approvals no longer automatically carried weight in the EU. EU regulatory approval must now be sought separately.

Financial services passporting: Before Brexit, UK financial services firms could “passport” their FCA authorisation across all EU member states, allowing them to serve EU clients without separate local licensing. That right ended on 31 December 2020. UK financial services firms that want to serve EU clients now need an EU-regulated entity.

Freedom of movement: UK nationals no longer have the automatic right to live and work across the EU, which creates complications for businesses with staff in multiple EU countries or businesses that want to employ EU-based talent.

None of these changes are temporary. They are the settled, long-term reality of the UK’s relationship with the EU.

Why Ireland Specifically? The Seven Reasons UK Businesses Choose Dublin

Given that there are 27 EU member states, you might reasonably ask why Ireland is the preferred destination for UK businesses seeking an EU base. The answer is not one reason it is a combination of factors that make Ireland uniquely well-positioned to serve as the EU home of UK-headquartered businesses.

1. The Only English-Speaking Country in the Eurozone

Since Brexit, Ireland is the only EU member state in the Eurozone where English is the primary business language. For UK businesses, this eliminates language barriers in legal documentation, regulatory correspondence, banking, and day-to-day operations. Your Irish solicitor, accountant, and bank manager all speak English. Your company documents are filed in English. Your Irish contracts are governed by English-language law.

2. Common Law Legal System

Ireland, like the UK, is a common law jurisdiction. Its corporate law, contract law, and commercial legal frameworks are closely aligned with UK equivalents. UK lawyers can navigate Irish legal structures with relative ease, and UK business owners find that the legal culture is familiar in a way that civil law countries France, Germany, the Netherlands simply are not.

3. The 12.5% Corporation Tax Rate

Ireland’s corporation tax rate of 12.5% on trading profits is one of the lowest in the developed world. The UK’s main corporation tax rate is 25% (for companies with profits above £250,000). For businesses routing EU trading profits through an Irish entity, the difference is material. Ireland’s corporation tax regime is compliant with OECD standards and is not going away it has been the cornerstone of Irish economic policy for decades and is politically embedded across party lines.

4. Full EU Single Market Membership

An Irish company is an EU company. It can sell goods and services across all 27 member states without customs friction, tariffs, or regulatory duplication. For businesses that sell into Europe, this restores the frictionless access that Brexit removed.

5. Geographic Proximity and Shared Time Zone

Dublin is approximately one hour by air from London. Ireland and the UK share a time zone. The physical and operational convenience of Ireland compared with, say, the Netherlands or Luxembourg is significant for businesses whose senior leadership remains UK-based.

6. Extensive Double Taxation Treaty Network

Ireland has double taxation agreements with 76 countries, including the United Kingdom, the United States, all EU member states, and most major trading nations. The Ireland-UK double taxation treaty specifically governs dividends, interest, and royalties flowing between the two jurisdictions, ensuring that profits generated by an Irish subsidiary are not subject to double taxation when repatriated to a UK parent.

7. Track Record and Infrastructure

Ireland has been attracting foreign direct investment for decades. Google, Apple, Meta, Microsoft, Pfizer, Johnson & Johnson, and hundreds of multinationals chose Ireland as their European base. The professional services infrastructure law firms, accountants, banks, talent that has grown up around that inward investment makes Ireland one of the most fully serviced business environments in Europe for international companies.

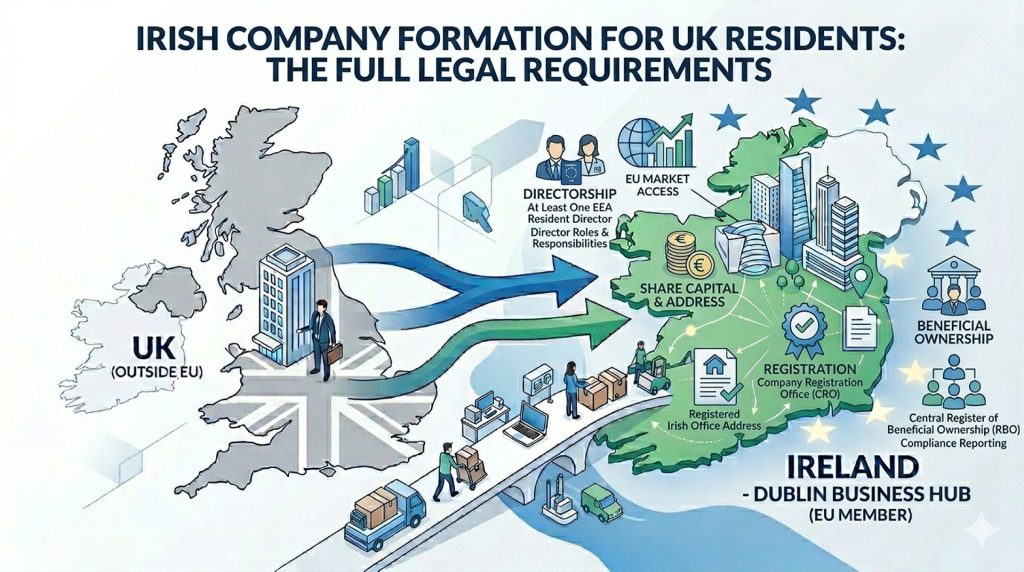

Irish Company Formation for UK Residents

Let us be specific about what is actually required to form an Irish company as a UK resident. This is where many guides get vague here is the complete picture.

Requirement 1: At Least One EEA-Resident Director

The Companies Act 2014 requires that at least one director of every Irish private limited company must be ordinarily resident in an EEA country. Since 1 January 2021, the UK is not an EEA country, which means UK residents do not satisfy this requirement.

You have two compliant options if you do not have an EEA-based director:

Option A: Appoint a Nominee EEA-Resident Director. A qualified, professional nominee director who is resident in an EEA country is appointed to your company. The nominee acts in accordance with a formal agreement that protects your control of the company. A reputable Irish company formation firm can provide this service.

Option B: Purchase a Section 137 Bond. A Section 137 Bond is an insurance policy taken out for a two-year period in the sum of €25,000. It is registered with the CRO and serves as a financial guarantee in lieu of an EEA-resident director. The bond must be renewed every two years for as long as the company has no EEA-resident director. The annual cost is typically a few hundred euros. The bond does not restrict your operation of the company in any way it is purely a compliance mechanism.

Which option is better depends on your specific structure, planned activities, and banking requirements. Some Irish banks look more favourably on companies with a physical Irish or EEA-resident director. For companies where banking relationships are critical, the nominee director route often makes more practical sense.

Requirement 2: A Registered Office Address in the Republic of Ireland

Every Irish company must maintain a registered office address within the Republic of Ireland. This is the official address to which all CRO and Revenue correspondence is sent. It must be a physical address not a PO box.

You do not need to occupy the address operationally. Many Irish companies including those run entirely from the UK use a virtual registered office address provided by a professional services firm. This is fully compliant under Irish company law.

Requirement 3: A Company Secretary

Every Irish company must have a company secretary. The secretary is responsible for ensuring the company meets its statutory compliance obligations annual returns, AGMs, filing deadlines, and so on. Where a company has only one director, the director and company secretary must be separate individuals or entities.

Requirement 4: VIN Numbers for Non-Resident Directors and Major Shareholders

Directors who are not resident in Ireland and do not have an Irish PPS number must obtain a Verification of Identity Number (VIN) from the CRO. Shareholders owning more than 25% of the company who are not Irish residents must also obtain a VIN.

The VIN process involves submitting certified identification documents to the CRO. A company formation firm can manage this on your behalf.

Requirement 5: A Unique and Compliant Company Name

Your chosen company name must be unique not identical or deceptively similar to an existing registered Irish company and must comply with CRO naming rules. Certain words (Bank, Insurance, Group, Holdings) require prior approval from specific regulators.

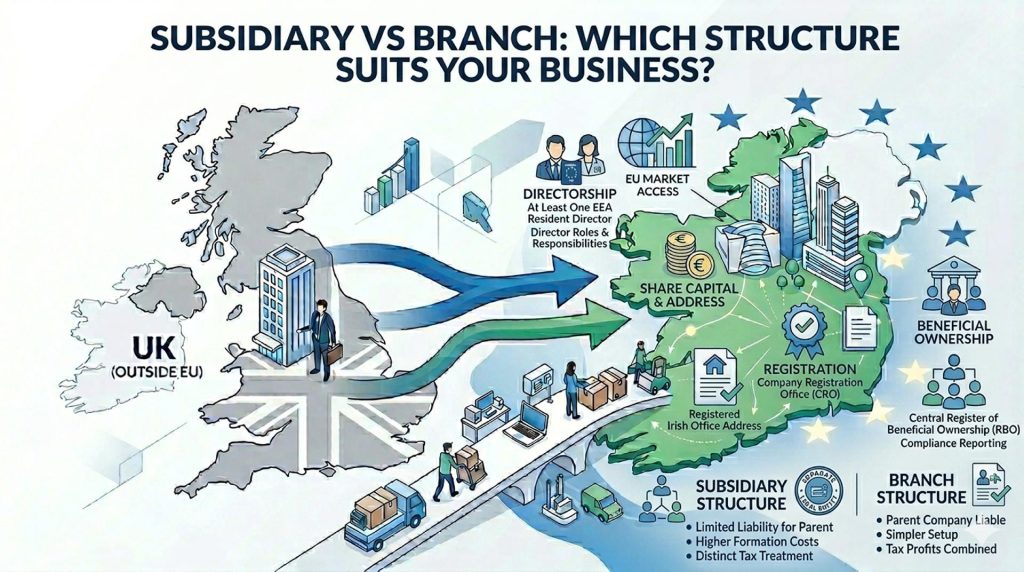

Subsidiary vs Branch Which Structure Suits Your Business?

For UK businesses establishing an Irish presence, the two most common structural options are a subsidiary (a new Irish private limited company) and a branch (a registered extension of the UK company). Here is an honest comparison.

The Subsidiary

A subsidiary is a new Irish company, incorporated under the Companies Act 2014, that is legally separate from the UK parent. The UK company typically holds the shares of the Irish subsidiary.

The subsidiary is liable for Irish corporation tax on all its worldwide profits. It maintains its own directors, company secretary, accounts, and annual filings in Ireland. Because it is a separate legal entity, it provides a clean barrier between the UK and Irish operations.

Advantages of the subsidiary structure:

Full EU market access as a standalone EU entity

Limited liability protection the UK parent’s exposure is limited to its investment in the Irish company

Clear and credible Irish corporate identity for clients, regulators, and partners

Potential to benefit fully from Ireland’s 12.5% corporation tax rate

Participation exemption on dividends received from subsidiaries and capital gains on disposal of shareholdings (subject to conditions)

The Branch

A branch is not a separate legal entity. It is the UK company operating in Ireland through a registered presence. It must be registered with the CRO as a branch of a foreign company, and it must have an authorised agent in Ireland.

Irish tax applies only to profits generated by the Irish branch’s activities not the UK company’s worldwide profits.

Advantages of the branch structure:

Simpler to establish no new corporate entity to maintain

Lower initial compliance cost

Useful where the Irish presence is operationally minor

Disadvantages:

The UK parent company bears full liability for the branch’s activities

Less attractive to EU clients and partners who may prefer a standalone Irish entity

Does not provide the same degree of structural separation as a subsidiary

More complex tax position in practice than it first appears

For the vast majority of UK businesses looking to establish a meaningful EU presence, the subsidiary structure is the appropriate and recommended choice. The branch is better suited to businesses that want a registered presence in Ireland with minimal operational activity.

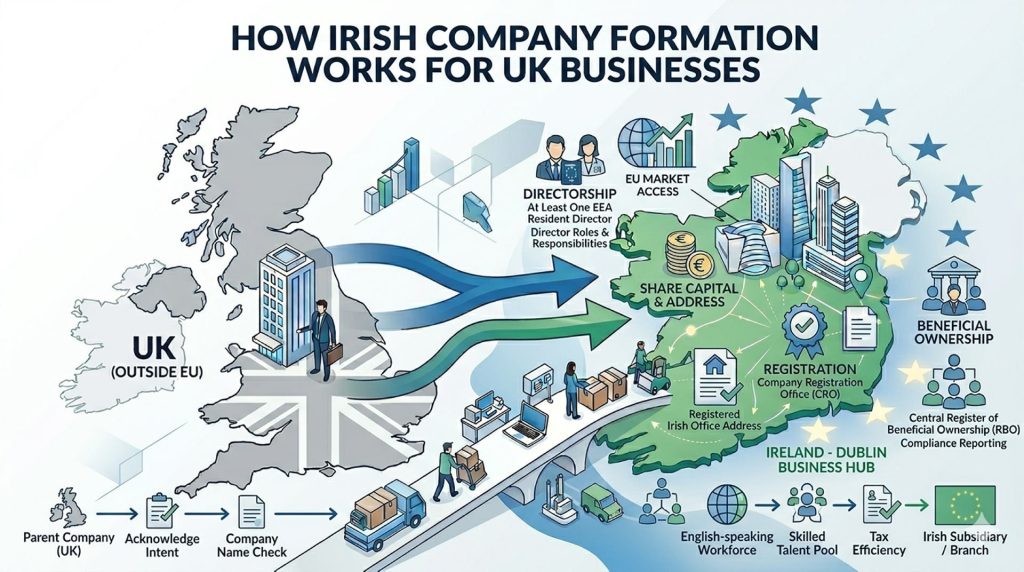

How Irish Company Formation Works for UK Businesses

Here is the actual process from initial decision to fully operational Irish company.

Step 1: Choose Your Structure: Decide between subsidiary and branch. If you are unsure, take professional advice the right structure depends on your planned activities, revenue profile, staffing plans, and banking needs. In most cases, a subsidiary is the right answer.

Step 2: Choose Your Company Name: Check availability against the CRO register. Your formation agent will do this on your behalf. Have two or three name options ready in case your first choice is unavailable.

Step 3: Appoint Directors and Satisfy the EEA Director Requirement: Decide who your Irish company directors will be. If no director is EEA-resident, arrange either a nominee EEA director or a Section 137 Bond.

Step 4: Appoint a Company Secretary: This can be an individual or a corporate body. Many Irish formation agents provide company secretarial services.

Step 5: Arrange a Registered Office Address: If you are not physically operating in Ireland, engage a professional registered office address service.

Step 6: Prepare and File Incorporation Documents: Your formation agent prepares and files Form A1 (the company registration form) and the company constitution (which replaces the old Memorandum and Articles of Association) with the CRO. Once filed, incorporation typically takes 3 to 5 business days.

Step 7: Obtain Your VIN Numbers: For non-resident directors and major shareholders, VIN applications are submitted to the CRO. Your formation agent manages this.

Step 8: Tax Registration: Once incorporated, your Irish company must register with Revenue for corporation tax. If the company will trade goods or services, VAT registration may also be required. If you plan to employ Irish-based staff, employer PAYE registration is necessary.

Step 9: Register of Beneficial Ownership (RBO) Filing: Ireland’s RBO requires all Irish companies to disclose their ultimate beneficial owners typically individuals who own more than 25% of the company. Your formation agent files this on your behalf.

Step 10: Open an Irish Business Bank Account: This is often the most time-consuming step in the process. Irish banks have KYC requirements that can be demanding for non-resident directors. Your formation agent should advise on which banks are most accessible and what documentation is required.

From start to finish, the company formation itself (Steps 1–7) typically takes one to two weeks for a straightforward structure. Tax registrations and banking can take a few additional weeks.

What UK Businesses Need to Understand

Corporation Tax

The headline rate is 12.5% on trading profits the rate that applies to the active business income generated by your Irish company. A 25% rate applies to passive income (rents, royalties where no active management is involved) and certain other non-trading income. Most UK businesses establishing an Irish trading entity will pay at the 12.5% rate.

Ireland’s corporation tax regime is OECD-compliant and participates in the OECD Pillar Two framework (a global minimum tax of 15% for large multinational groups with revenues above €750 million). For the vast majority of UK businesses, Pillar Two is not relevant.

VAT in Ireland

Ireland’s standard VAT rate is 23%. A reduced rate of 13.5% applies to certain categories including construction, tourism, and some professional services. The 0% rate applies to certain goods and to most international services.

If your Irish company will supply taxable goods or services within Ireland, VAT registration is required once the relevant turnover threshold is reached. If your Irish company will supply services to EU business customers in other member states, the reverse charge mechanism typically applies and no Irish VAT is charged.

The Ireland-UK Double Taxation Agreement

The double taxation agreement between Ireland and the UK governs the tax treatment of cross-border payments between Irish and UK entities. Under this treaty:

Dividends paid from your Irish subsidiary to your UK parent are generally exempt from withholding tax where the UK parent holds a significant shareholding

Interest payments between the two companies are subject to a maximum 0% withholding tax rate

Royalty payments are subject to agreed reduced withholding rates

This agreement ensures that your profits are not taxed twice once in Ireland and once in the UK when they flow between the two companies.

Irish vs UK Tax Rate Comparison

Tax

Ireland

UK

Corporation tax (trading)

12.5%

25% (above £250k profits)

Corporation tax (small profits)

12.5%

19% (below £50k)

Capital gains tax (companies)

33%

25%

Standard VAT rate

23%

20%

Dividend withholding tax (to treaty countries)

25% (reduced/exempt under treaties)

0% (after tax credit)

E-Commerce and Digital Businesses

For UK e-commerce businesses selling to EU consumers, Brexit created a particular set of complications around VAT. Since July 2021, the EU’s One Stop Shop (OSS) scheme allows businesses to register for VAT in a single EU member state and account for VAT across all EU member states through a single return.

An Irish company can register for the EU OSS in Ireland, simplifying VAT compliance across all 27 member states. This eliminates the need to register for VAT separately in each country where you have customers a significant administrative and cost saving for businesses selling at scale across Europe.

For goods sold to EU consumers, Ireland’s membership of the EU Single Market means goods can move freely between Ireland and other EU member states without customs declarations or import duties. Goods moving from the UK to your Irish subsidiary and then to EU customers travel the UK-to-Ireland leg only once after which they move within the EU without friction.

Passporting, Authorisation, and Ireland’s Regulatory Framework

For UK financial services firms, Brexit meant the loss of EU passporting rights the mechanism that previously allowed FCA-authorised firms to serve clients across the EU without separate licensing in each member state.

Ireland’s financial services regulator, the Central Bank of Ireland (CBI), has become the EU regulatory authority of choice for many UK financial firms looking to re-establish EU market access. The reasons are familiar: English language, common law system, proximity, and a regulator that has demonstrated capacity and commercial pragmatism in handling the significant volume of relocations that followed Brexit.

Establishing a CBI-authorised entity in Ireland requires:

A genuine substance commitment staff, systems, and governance actually located in Ireland

Regulatory capital appropriate to the licence type sought

A credible senior management team with relevant experience

Compliance infrastructure that meets CBI expectations

TAS Consulting works alongside specialist financial services regulatory advisors for firms in this position. We handle the company formation and ongoing accounting, secretarial, and tax functions while ensuring your regulatory preparation is properly coordinated.

UK Businesses Make When Setting Up in Ireland

Underestimating the genuine substance requirement

Revenue and the CBI both look unfavourably on arrangements where an Irish company exists on paper but has no real presence, management, or decision-making in Ireland. For tax purposes, an Irish company must be managed and controlled in Ireland to be treated as Irish tax resident. If all decisions are actually made in the UK, the Irish company may be regarded as UK tax resident defeating the purpose of the structure. Genuine Irish substance matters.

Choosing the wrong structure at the outset

Setting up a branch when a subsidiary was appropriate or vice versa creates complications that are expensive to unwind. Take proper advice before you start.

Not planning the banking relationship

Irish business banking for non-resident directors is more demanding than many UK business owners expect. Some banks require in-person meetings, have extensive KYC requirements, and can take several weeks to open accounts. Plan for this in advance.

Ignoring the EEA director requirement

This is the most commonly overlooked requirement. Companies formed without properly satisfying the EEA director requirement are non-compliant from day one. The CRO can strike off non-compliant companies.

Confusing Irish formation with Irish tax residency

Forming a company in Ireland does not automatically make it Irish tax resident. Tax residency is determined by where the company is managed and controlled where the board actually meets and makes decisions. For the structure to deliver its intended benefits, genuine Irish management and control must be established.

Start Your Business Journey Now

Hundreds of startups already growing with TAS Consulting

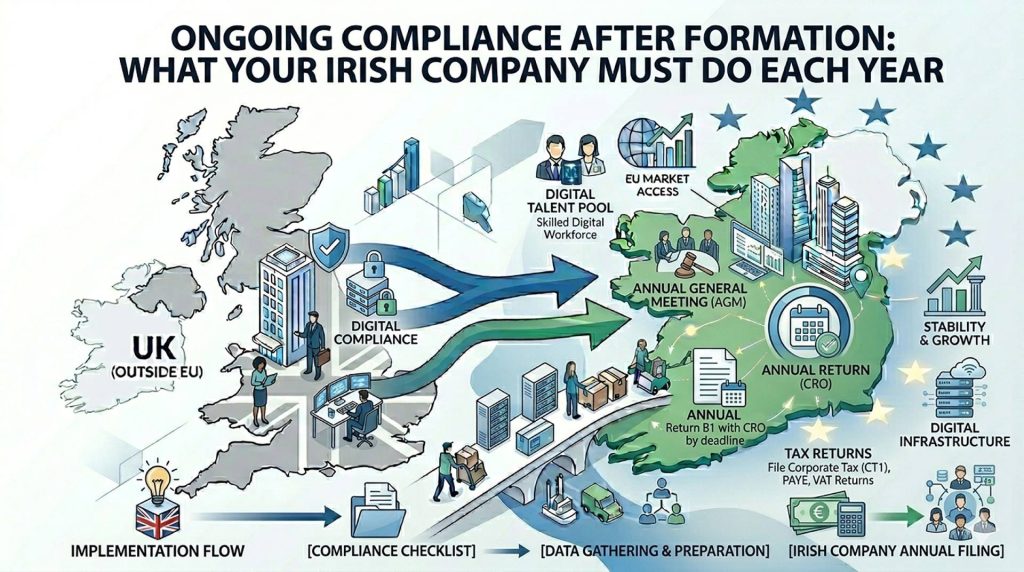

Ongoing Compliance After Formation What Your Irish Company Must Do Each Year

Forming the company is step one. Keeping it compliant is an ongoing obligation. Here is what Irish companies are required to do annually:

Annual Return to the CRO

Every Irish company must file an annual return with the CRO. The return includes basic company information (directors, registered office, shareholders) and financial statements (for most companies). The annual return deadline is typically 28 days after the company’s Annual Return Date (ARD). Late filing attracts penalties and, for persistent non-compliance, can result in the company being struck off.

Financial Statements

Irish companies must prepare financial statements in accordance with Irish GAAP or IFRS. Small companies qualify for reduced disclosure requirements. Financial statements are filed with the CRO as part of the annual return.

Corporation Tax Return

The corporation tax return (Form CT1) must be filed with Revenue within nine months of the company’s financial year end. Preliminary tax is due on a pay-and-file basis throughout the year.

VAT Returns

If registered for VAT, your company must file periodic VAT returns (typically bi-monthly) and make corresponding payments to Revenue.

Payroll and Employer Obligations

If your Irish company employs staff, PAYE real-time reporting is required for every pay period under Revenue’s PAYE Modernisation system.

Register of Beneficial Ownership (RBO)

Updates to beneficial ownership must be filed with the RBO within 14 days of any change.

TAS Consulting provides ongoing company secretarial, accounting, and tax compliance services to ensure all of these obligations are met on time, every year.

The Strategic Case for an Irish Company Has Never Been Clearer

Brexit is not going to be reversed. The UK-EU trade and regulatory relationship is settled, and the friction it creates for UK businesses operating in or trading with Europe is permanent.

For businesses of a certain size and ambition, absorbing that friction indefinitely is not a strategy it is a slow erosion of competitive advantage. The businesses that are prospering in this environment are the ones that have taken a clear-eyed look at their EU exposure and put the right structure in place to manage it.

Ireland offers the most accessible, most commercially rational, and most operationally convenient route back into the EU for UK businesses. It is English-speaking, legally familiar, geographically close, tax-competitive, and genuinely open for business.

TAS Consulting has helped UK businesses establish Irish companies of every size and in every sector. We know the process, the requirements, the pitfalls, and the opportunities. If you are considering your options, the first step is a conversation.

Talk to TAS Consulting About Your Irish Company

Whether you are starting from scratch or restructuring an existing business for the post-Brexit world, TAS Consulting handles the entire process from company formation and tax registration to ongoing secretarial compliance and accounting.

Trusted Experts in Company Formation and Business Support

Brexit company formation Ireland guide

This guide simplifies Irish company formation for UK-based businesses post-Brexit. It details essential compliance steps, including the Section 137 Bond for non-EEA directors, the Verified Identity Number (VIF) process, and leveraging the 12.5% corporation tax. Ireland remains the premier, English-speaking hub for seamless access to the European Single Market.