✓ Meets Irish EEA director compliance requirements ✓ Revenue-approved non-resident director bond included ✓ Full documentation and CRO filing support ✓ Fast and hassle-free setup process ✓ Secure handling of all legal records ✓ Ongoing compliance and advisory support

This guide is for company directors, business owners, solicitors, and accountants who need to understand how company re-registration works in Ireland either because they are considering converting their own company to a different type, or because they advise clients who are.

If you are unsure whether re-registration applies to your situation, or you want to understand the legal process, the documents required, and the practical implications before taking any steps, this guide gives you everything you need in plain, accurate language.

In this guide, you’ll find:

A clear explanation of what company re-registration is and how it works under the Companies Act 2014

A full breakdown of every permitted re-registration route LTD, DAC, PLC, CLG, and ULC

The specific requirements, resolutions, and CRO forms involved in each conversion

Practical guidance on what changes and what stays the same after re-registration

The most common reasons businesses re-register and how to decide if it is right for you

Common mistakes and how to avoid them

Key Takeaways

Re-registration converts an existing Irish company from one type to another under Part 20 of the Companies Act 2014 the same legal entity continues, the CRO number stays the same, and existing contracts and obligations are unaffected

The process requires a special resolution (75% member approval in most cases, 100% for conversion to unlimited), a new constitution, the correct CRO form, and a compliance statement

Different re-registration routes carry specific additional requirements particularly for PLC conversions (minimum share capital), CLG conversions (possible court order), and ULC conversions (financial statements must be filed first)

A compliant service provider should review your constitution, prepare all documents correctly, file with the CRO, and advise on all post-registration steps not just process a single form

Why Irish Companies Re-Register

A company’s legal structure is not permanent. What made sense when a business was first incorporated may not suit it five or ten years later. The owner-managed LTD that once served a small business perfectly may need to become a DAC when investors require defined company objects. The PLC that once sought public capital may want to return to a simpler private structure. The trading company whose founders now want to transition to a charitable purpose needs to become a CLG.

Re-registration exists to make these transitions possible without the disruption and cost of winding up one company and forming another. It is one of the most practical and underused tools in Irish company law and under the Companies Act 2014, it is more flexible than ever.

This guide explains every aspect of the process what it is, who it applies to, what each conversion route involves, and how to get it right.

What Is Company Re-Registration Under Irish Law?

Re-registration is the formal legal process by which an Irish company converts from one company type to another. It is governed by Part 20 of the Companies Act 2014, specifically Sections 1283 to 1299.

The key principle is continuity. When a company re-registers, it does not cease to exist and reform as a new entity. The same company continues with the same CRO registration number, the same directors, the same shareholders, the same contracts, and the same legal obligations. What changes is the company type under which it operates.

The Companies Act 2014 significantly expanded and streamlined the re-registration framework compared to the previous legislation. In particular, it introduced the ability for an Unlimited Company to re-register as a Limited Company something that was previously prohibited and it created clearer pathways between all company types.

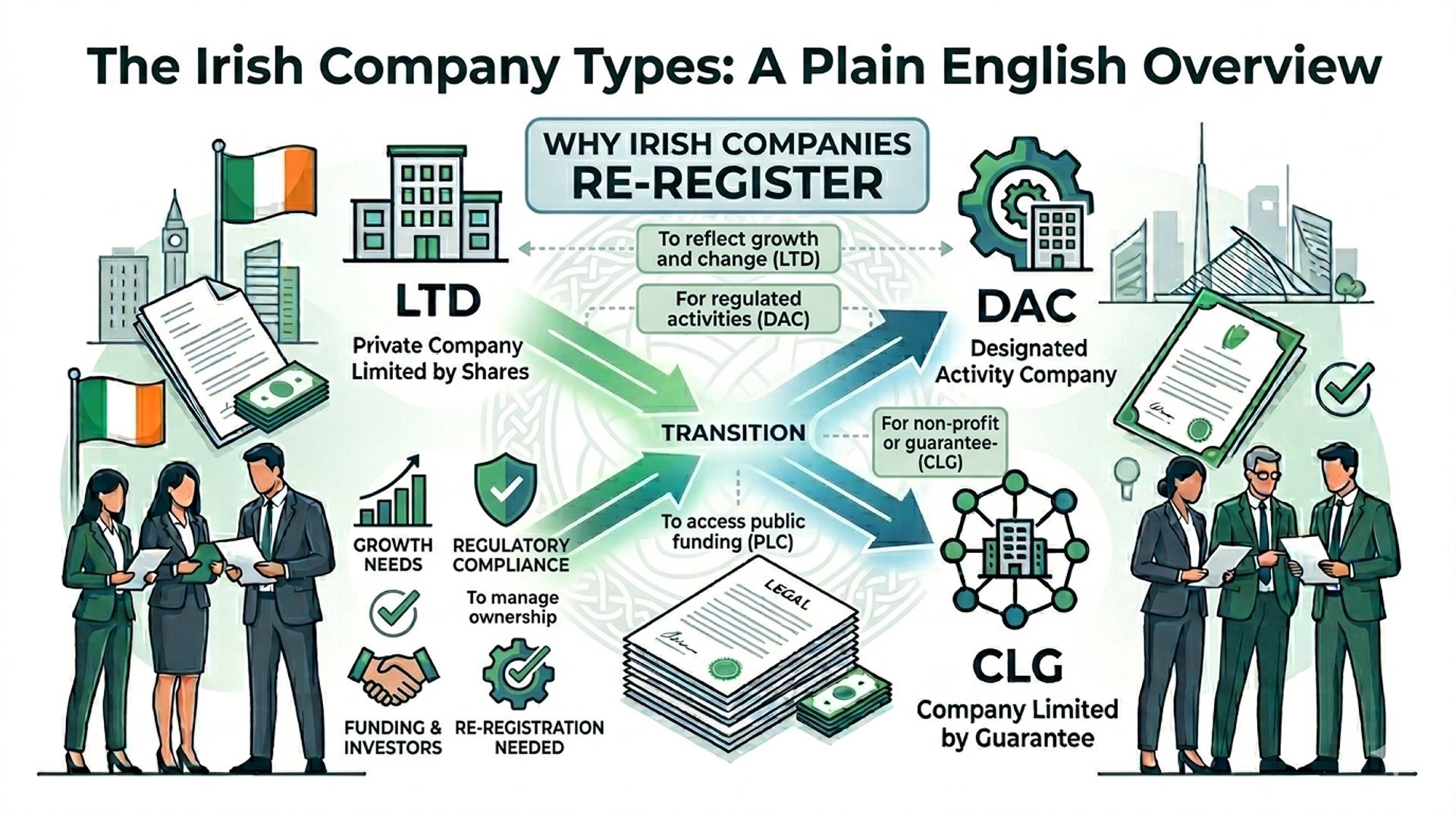

The Irish Company Types A Plain English Overview

Before exploring the re-registration routes, it helps to understand clearly what each company type is and who uses it.

LTD: Private Company Limited by Shares The most widely used company type in Ireland. A private company with a minimum of one director, limited liability for members, no requirement to hold an AGM, and no requirement for a written constitution with defined objects. Suited to most owner-managed and small-to-medium businesses.

DAC: Designated Activity Company A private company, also limited by shares or by guarantee, that must have a specific objects clause in its constitution limiting the scope of what it can do. This makes the DAC suitable for joint venture companies, special purpose vehicles, companies holding specific licences, and situations where investors or lenders require certainty about the company’s activities.

PLC: Public Limited Company A company whose shares can be offered to the public and traded on a stock exchange. Requires a minimum share capital of €38,092.14 (at least 25% paid up), at least two directors, a formally qualified company secretary, public financial disclosure, and an annual general meeting. Used by listed companies and those preparing for a public offering.

CLG: Company Limited by Guarantee A company with no share capital. Members provide a guarantee typically a nominal amount rather than holding shares. The CLG structure is used by charities, non-profit organisations, sports clubs, professional associations, and membership bodies where there is no intention to distribute profits to members.

ULC: Unlimited Liability Company A company where members have unlimited personal liability for the company’s debts. The key practical attraction is that ULCs are not required to file their financial statements publicly with the CRO making them suitable for businesses that wish to keep financial information private. Used by subsidiaries of multinationals, family businesses, and certain professional firms.

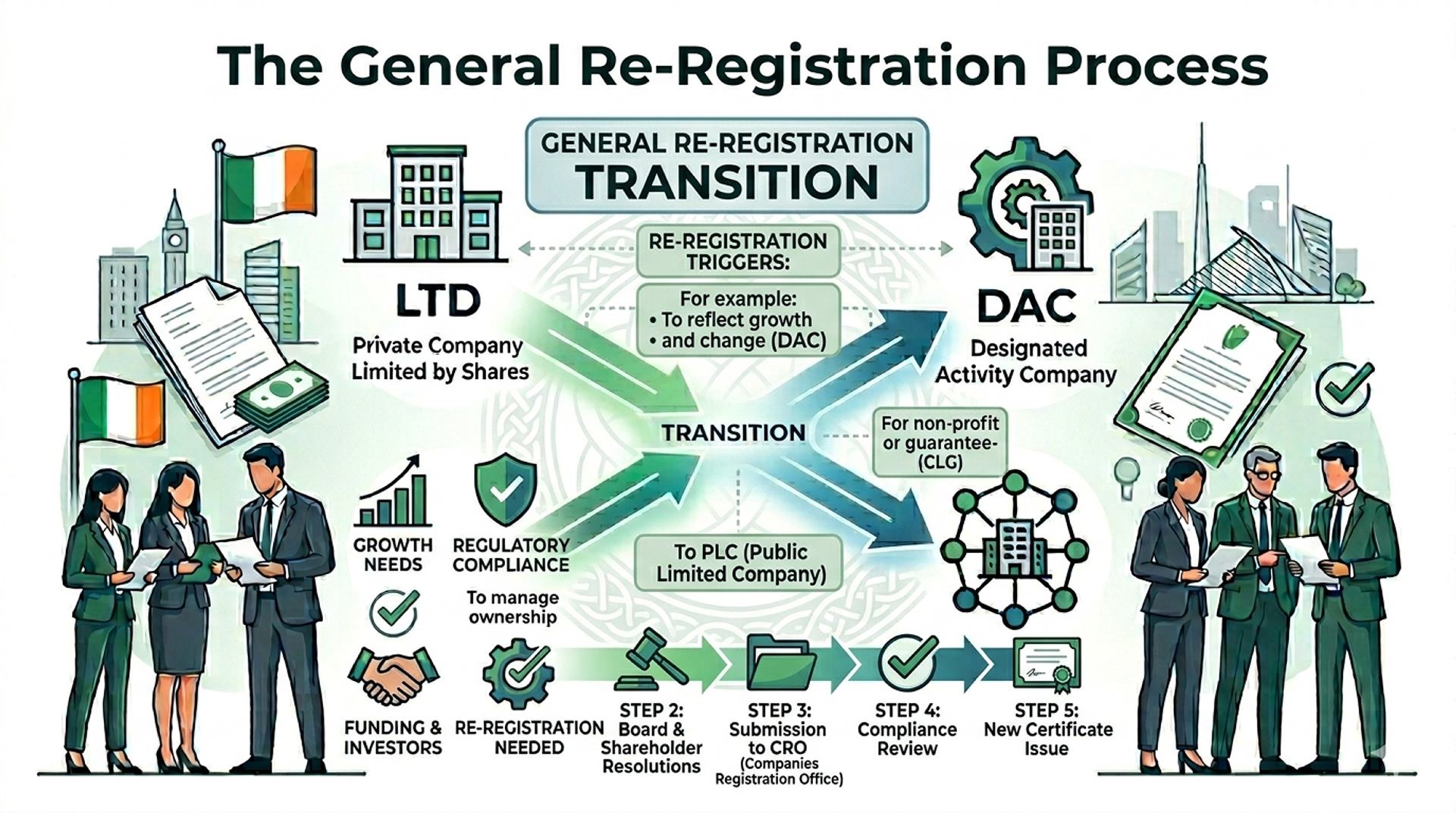

All Re-Registration Routes Under the Companies Act 2014

Part 20 of the Companies Act 2014 provides for re-registration between all company types. Here is a complete breakdown of each route, the legal basis, and what it involves.

LTD to DAC

An LTD re-registers as a DAC primarily when the company’s activities need to be formally restricted typically at the request of investors, lenders, or regulators who require certainty about what the company can and cannot do.

The process involves passing a special resolution, adopting a DAC constitution with a defined objects clause, and filing the appropriate CRO form with a compliance statement. The DAC constitution must specify the company’s objects the range of activities it is authorised to carry on.

An LTD may also be converted to a DAC involuntarily Section 63 of the Companies Act 2014 provides that if a majority of shareholders holding at least 25% of voting rights give notice requiring the company to convert, the board must convene a general meeting to do so.

LTD to PLC

Re-registering as a PLC is the route taken by companies preparing for a public share offering or a stock exchange listing.

The LTD must satisfy specific conditions at the time of re-registration. Allotted share capital must be not less than €38,092.14, with at least 25% paid up. The company must have a minimum of two directors. The company secretary must meet the qualifications required for a PLC secretary under the Companies Act. A qualified professional must prepare a report confirming that the company’s net assets are not less than the aggregate of its called-up share capital and undistributable reserves.

A special resolution of members is required, along with a new PLC constitution and the appropriate CRO form. Once re-registered, the company is subject to the full range of PLC obligations AGM, public financial disclosure, and compliance with any relevant stock exchange rules.

LTD to CLG

An LTD converts to a CLG most commonly when a trading company transitions to a charitable or non-profit purpose, or when founders want to relinquish the shareholding structure in favour of a membership model.

This is one of the more complex re-registration routes. An LTD that has paid-up share capital cannot re-register directly as a CLG it must first obtain a High Court order under Section 1297(2)(c) of the Companies Act 2014 authorising the conversion and giving directions as to how the share capital is to be treated. Where the LTD has no paid-up share capital, the High Court application may not be required.

The new CLG constitution replaces the LTD constitution, and the company adopts a guarantee structure under which members agree to contribute a nominal amount (usually €1) in the event of a winding up.

LTD to ULC

An LTD converts to an Unlimited Liability Company (ULC) primarily to achieve privacy of financial information. Once re-registered as a ULC, the company is no longer required to file financial statements with the CRO for public inspection.

This route requires unanimity every single member of the company must consent to the re-registration. A single dissenting member can block the conversion. This reflects the seriousness of the change in liability position for members.

The company must also have filed financial statements with the CRO within the three months preceding the application or must file them as part of the process. This requirement prevents companies from switching to unlimited status specifically to conceal financial difficulties.

DAC to LTD

A DAC re-registers as an LTD when the objects clause restriction is no longer required for example, after a joint venture concludes, a licence expires, or an investor exits and removes their requirement for a defined scope of activity.

This route is more straightforward than most. A special resolution is passed, a new LTD constitution (without a defined objects clause) is adopted, and the CRO form and compliance statement are filed. The LTD has no mandatory objects clause and is presumed to have full legal capacity so the conversion removes the constitutional restriction entirely.

PLC to LTD or DAC

A PLC that wishes to step back from public company status after a delisting, a buyout of public shareholders, or a decision to return to private ownership re-registers as either an LTD or a DAC.

Minority shareholders in a PLC have a right of objection. Shareholders holding at least 5% of the nominal value of any class of issued share capital, or at least 50 members who have not voted in favour of the re-registration resolution, can apply to the High Court to cancel the re-registration within 28 days of the resolution being passed. If no such application is made within the 28-day period, the CRO filing proceeds.

CLG to DAC

A CLG may re-register as a DAC when the organisation decides to introduce share capital for example, a previously guarantee-only organisation that wants to raise equity or restructure for commercial purposes.

This involves transitioning from a no-share-capital structure to a share capital structure, which requires careful preparation of a statement of share capital and initial shareholdings, in addition to the special resolution, new constitution, and CRO form.

ULC to LTD

Under the old Companies Acts, a company that had re-registered as unlimited was prohibited from subsequently re-registering as limited. The Companies Act 2014 removed this prohibition.

An unlimited company may now re-register as a limited company, provided it files financial statements before making the application. This makes the ULC route genuinely reversible, which has made the structure more attractive to businesses that want to use it for a defined period.

Regardless of which re-registration route applies, the process follows a consistent structure.

Step 1: Assess the Current Position Review the company’s constitution, share capital, membership structure, and any shareholder agreements or third-party restrictions. Identify any preconditions such as the ULC financial statements requirement or the PLC net assets test that must be satisfied before proceeding.

Step 2: Obtain Member Approval Pass a special resolution at a general meeting of the members. For most re-registrations, this requires at least 75% of votes cast to be in favour. For conversion to a ULC, 100% unanimous consent is required.

Step 3: Draft the New Constitution Prepare a new constitution appropriate to the target company type. This is a full constitutional document not simply an amendment to the existing one. The new constitution must comply with the Companies Act requirements for the target type.

Step 4: Prepare the CRO Form and Compliance Statement Complete the relevant CRO re-registration form. A compliance statement confirming that all conditions for re-registration have been met must accompany the filing.

Step 5: File with the CRO Submit the special resolution, new constitution, CRO form, and compliance statement to the Registrar of Companies. The Registrar reviews the documents and, if satisfied, issues a new Certificate of Incorporation on Re-Registration.

Step 6: Post-Registration Updates Update Revenue records, banking mandates, company letterheads, email signatures, website references, and any contracts or licences that reference the company type. Notify relevant regulators if the company operates in a regulated sector.

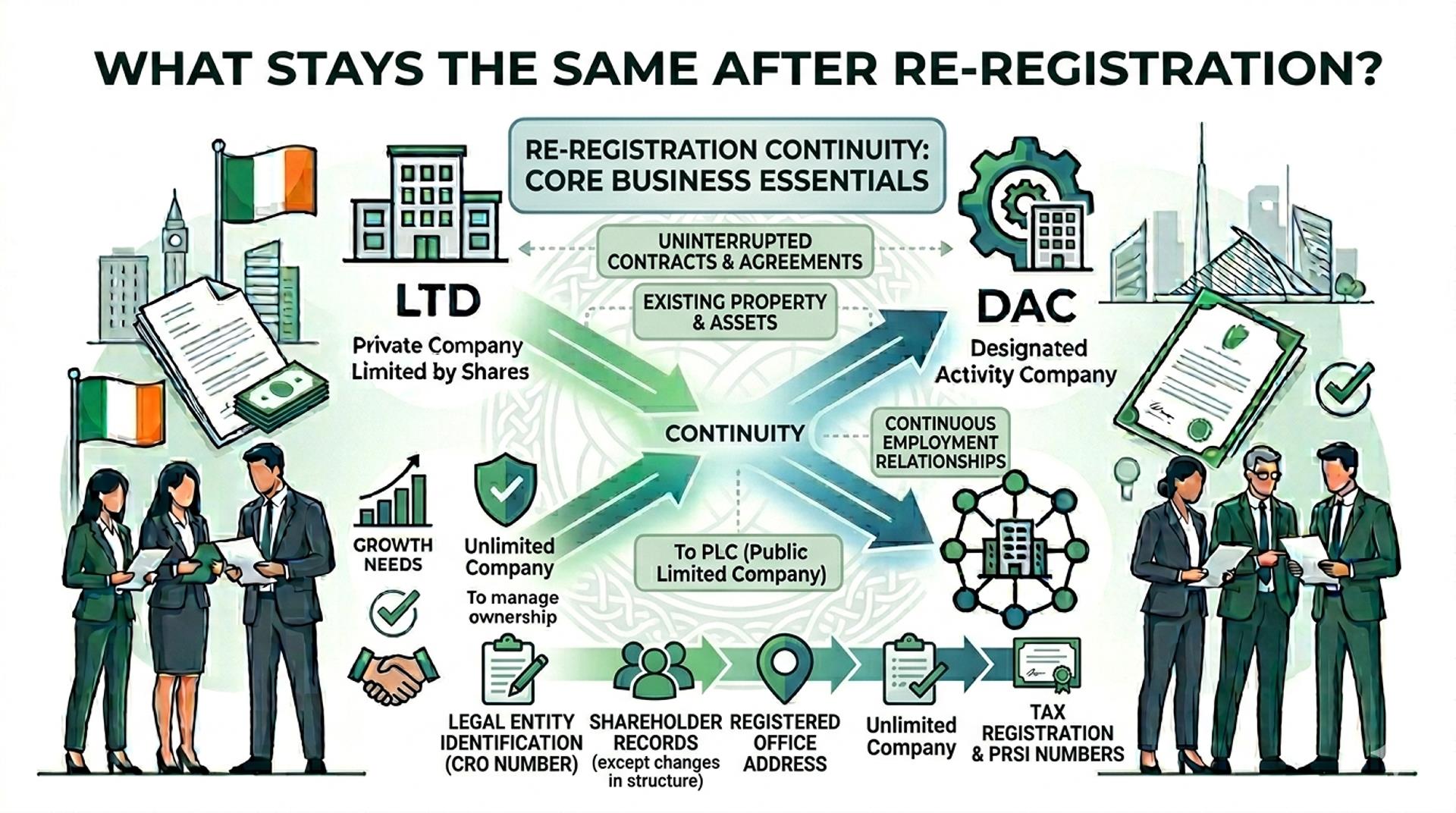

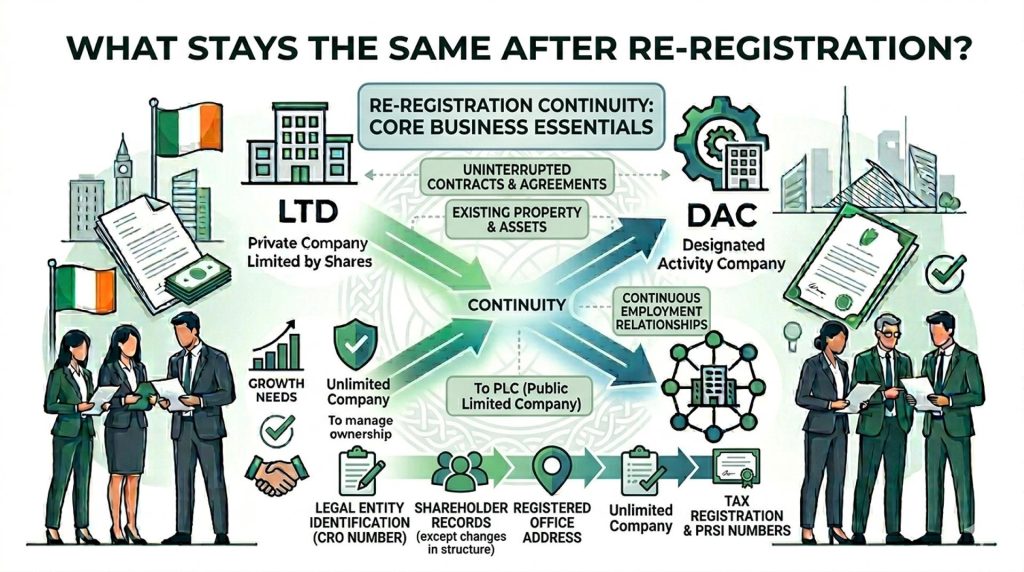

What Stays the Same After Re-Registration

This is the question that concerns most business owners considering re-registration. The answer is reassuring.

Under Section 1284 of the Companies Act 2014, re-registration does not affect the rights or obligations of the company. Specifically:

The company retains the same CRO number it is the same legal entity

All existing contracts remain fully valid without any need for re-execution

Legal proceedings against the company in its former type continue against it in its new type

Employees are not affected there is no transfer of employment

Tax registrations continue corporation tax, VAT, and employer PAYE registrations all carry through

Bank accounts are not disrupted though the company type on the mandate should be updated

The only material change is the company type on the CRO register and the Certificate of Incorporation.

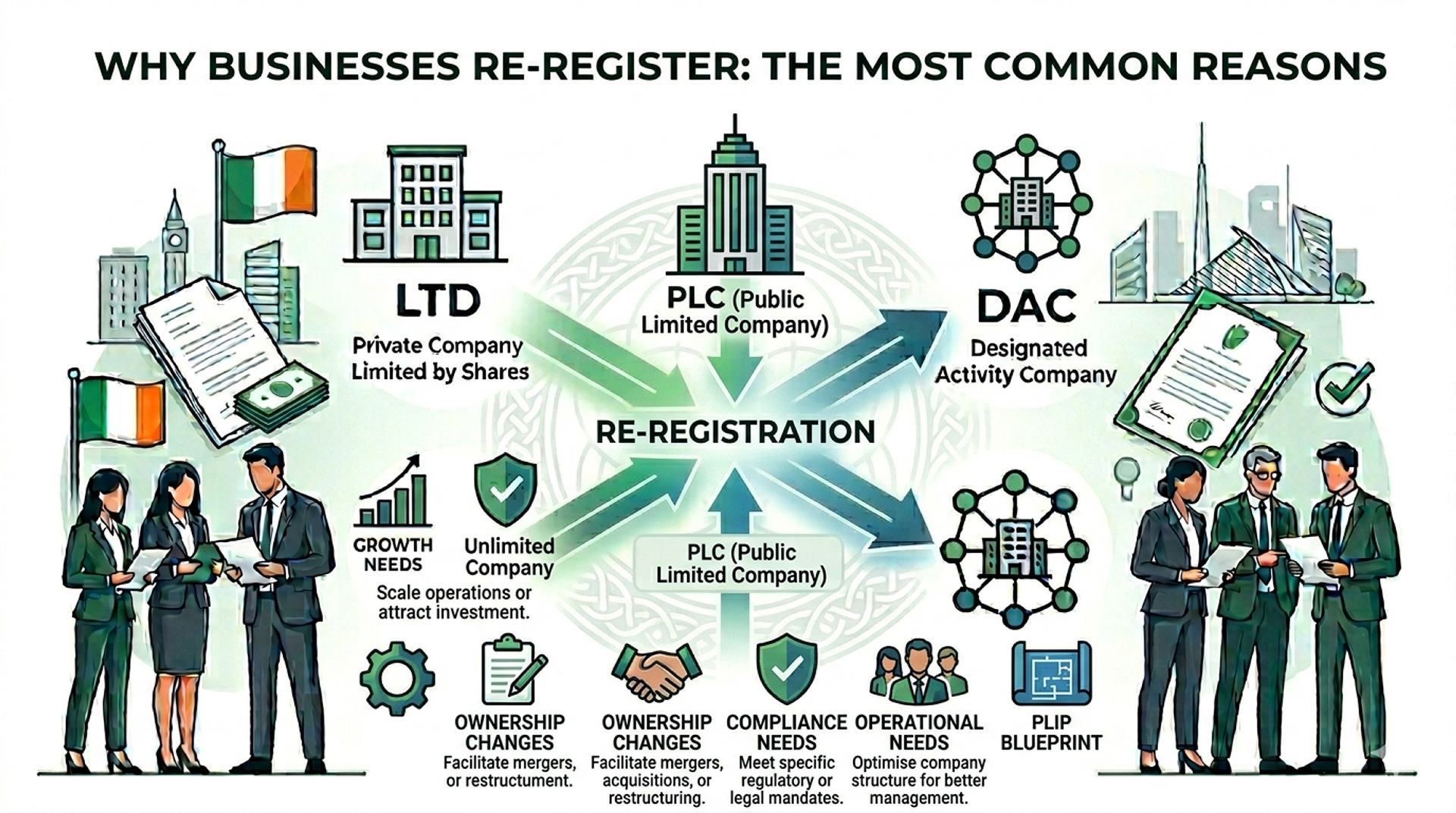

Why Businesses Re-Register The Most Common Reasons

Understanding the practical reasons behind re-registration helps identify whether it applies to your situation.

LTD to DAC: Investor and lender requirements. Investors and lenders taking a stake in or providing debt to an Irish company frequently require it to operate as a DAC with defined objects. This protects their investment by ensuring the company cannot stray beyond its agreed scope of activity.

LTD to ULC: Financial privacy. Family businesses, subsidiaries of multinationals, and professional firms that do not need or want their financial information on public record at the CRO use the ULC structure. The trade-off unlimited personal liability for members is acceptable to them given the privacy benefit.

LTD to CLG: Charitable conversion. Trading companies whose founders want to transition to a charitable or not-for-profit model use the CLG route. This is increasingly common in social enterprise, community sport, and arts organisations.

LTD to PLC: Capital raising. Companies preparing for an IPO or seeking to list on a stock exchange must first re-register as a PLC. This is the mandatory structural step before any public share offering.

PLC to LTD: Going private. Companies that have delisted or been taken private through a buyout re-register as LTDs to shed the compliance overhead of PLC status.

DAC to LTD: Removing restrictions. Companies that were previously required by investors or lenders to operate as a DAC re-register as an LTD when that requirement falls away simplifying governance and removing the constitutional limitations.

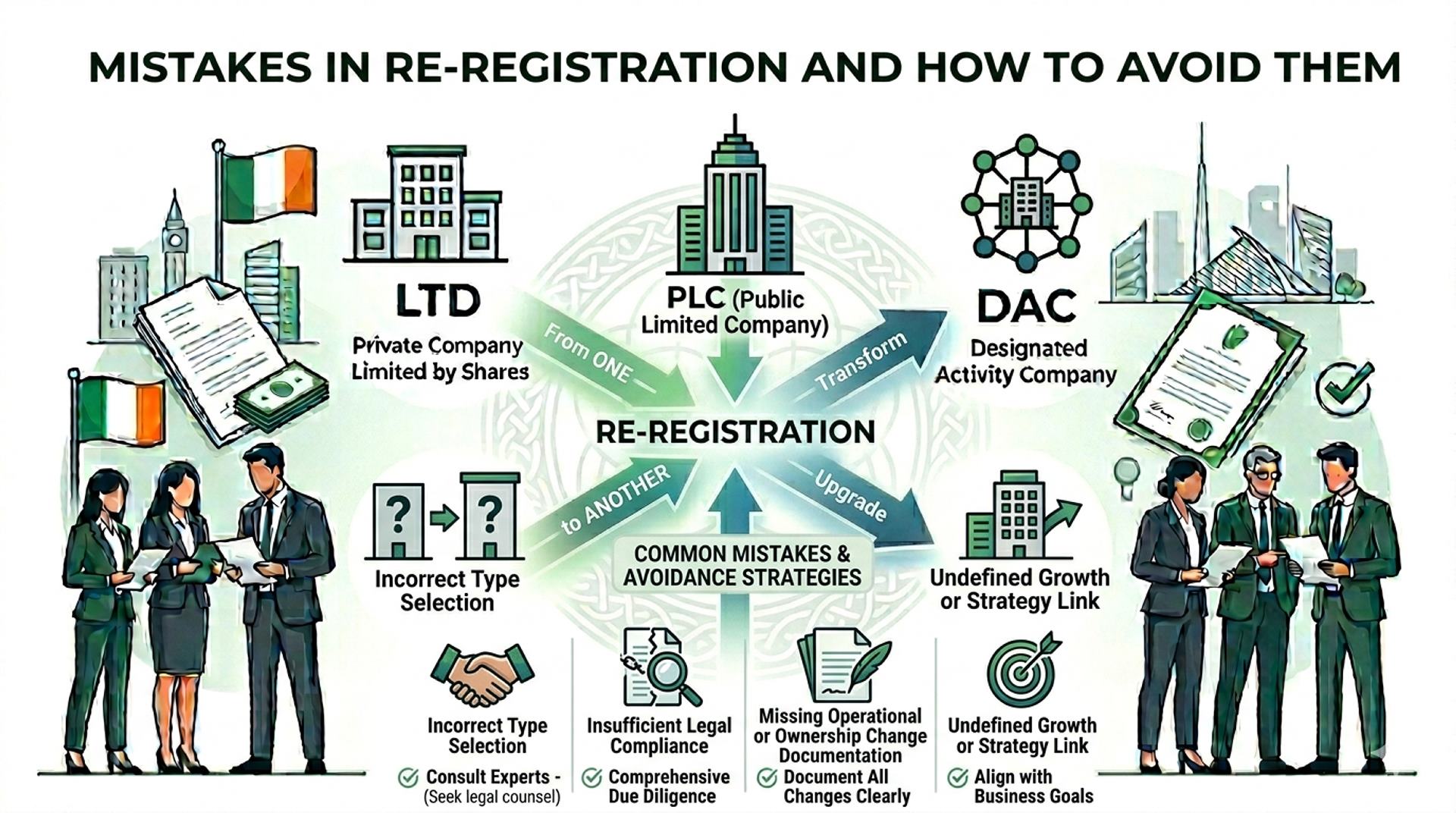

Mistakes in Re-Registration and How to Avoid Them

Proceeding without reviewing the company constitution first: The existing constitution governs the re-registration process who has the authority to call a meeting, what approval thresholds apply, and whether any shareholder has specific rights that affect the process. Missing this step leads to resolutions that may be invalid.

Using the wrong approval threshold: Most re-registrations require a 75% special resolution. Conversion to a ULC requires 100% unanimous consent. Using the wrong threshold invalidates the resolution.

Preparing an incomplete or incorrect new constitution: The new constitution must fully comply with the requirements of the Companies Act for the target company type. An LTD constitution used for a DAC (or vice versa) is a compliance failure from day one.

Failing to satisfy preconditions: For ULC conversions, financial statements must be filed first. For PLC conversions, the net assets test must be met. For CLG conversions, the share capital position must be assessed and a court application may be needed. Missing preconditions results in the CRO refusing the application.

Not updating post-registration records: Once re-registration is complete, Revenue, banks, regulators, and key counterparties should be informed. Companies that fail to do this create confusion and potential compliance issues down the line.

Re-Registration vs Forming a New Company Which Is Right?

Sometimes the question arises whether it is better to re-register an existing company or wind it up and form a new one. The answer depends on the specific circumstances, but re-registration is almost always preferable when:

The existing company has valuable contracts, licences, or trading history

The company has employees whose continuity of employment you want to maintain

The company has established banking relationships and credit facilities

The company has an existing tax compliance record that is clean and settled

Forming a new company makes more sense only when the existing company has liabilities, reputational issues, or structural problems that you want to leave behind and even then, those issues may follow the directors personally regardless of the company structure.

Re-Registration Is the Efficient Path to a Better Structure

Re-registration under the Companies Act 2014 is a well-established, legally sound process that allows Irish companies to evolve their structure as their business evolves without the cost and disruption of winding up and reforming.

If your current company type no longer fits your business model, your investor requirements, or your long-term plans, re-registration is almost certainly the right tool. The process is not complicated when handled correctly but getting the documents right, satisfying any preconditions, and ensuring the CRO filing is complete matters significantly.

TAS Consulting manages re-registrations for Irish companies of every type. We handle the process from initial assessment to Certificate of Incorporation on Re-Registration correctly, efficiently, and with full compliance at every step.

Start Your Business Journey Now

Hundreds of startups already growing with TAS Consulting