✓ Meets Irish EEA director compliance requirements ✓ Revenue-approved non-resident director bond included ✓ Full documentation and CRO filing support ✓ Fast and hassle-free setup process ✓ Secure handling of all legal records ✓ Ongoing compliance and advisory support

This guide is for Irish business owners, sole traders, contractors, and company directors who want to understand virtual bookkeeping what it is, how it works in practice, what it costs, and whether it is the right solution for their business.

If you are currently doing your own books, considering switching from an in-house bookkeeper, or simply trying to understand how cloud-based bookkeeping fits into Irish Revenue compliance, this guide gives you a clear, practical answer.

In this guide, you’ll find:

A plain English explanation of what virtual bookkeeping is and how it differs from traditional bookkeeping

How virtual bookkeeping works with Irish Revenue requirements VAT, PAYE, RCT, and corporation tax

The cloud accounting tools most widely used by Irish businesses and bookkeepers

A cost comparison between virtual bookkeeping and hiring in-house

How to switch to virtual bookkeeping without disrupting your business

The questions to ask before choosing a virtual bookkeeping provider in Ireland

Key Takeaways

Virtual bookkeeping is professional bookkeeping delivered entirely online the same accuracy and compliance as in-house, without the salary, PRSI, or management overhead

Irish businesses using virtual bookkeeping must still meet all Revenue obligations VAT3 returns, PAYE Modernisation, RCT, and annual CRO filings a good virtual bookkeeper handles all of these

Cloud accounting software (Xero, QuickBooks, Sage, FreeAgent) is the operational backbone of virtual bookkeeping real-time data access means you always know where your business stands financially

For most Irish SMEs, virtual bookkeeping costs significantly less than an equivalent in-house hire while delivering broader expertise and more consistent compliance

Choosing an Irish-based provider with specific knowledge of Revenue rules, Irish VAT law, and CRO obligations is essential generic international providers often miss Ireland-specific requirements

Why Irish Business Owners Are Moving Their Books Online

Running a business in Ireland has always involved paperwork. VAT returns every two months. Payroll submissions every pay period. Annual accounts for the CRO. Income tax returns. RCT for anyone in construction. The list of compliance obligations has not shortened if anything, Revenue’s PAYE Modernisation system has made real-time payroll reporting a permanent feature of Irish business life.

What has changed is how you can manage all of that paperwork. Cloud accounting software, secure document sharing, and remote professional services have made it possible to have your books kept to the same professional standard as a large company without hiring a full-time bookkeeper, without filling a filing cabinet, and without being tied to a single physical office.

Virtual bookkeeping is the practical result of that shift. And for a growing number of Irish businesses from sole traders in Cork to limited companies in Dublin it is now simply the way their accounts are run.

What Is Virtual Bookkeeping? A Plain English Definition

Snippet-ready answer: Virtual bookkeeping is the remote management of a business’s financial records by a professional bookkeeper using cloud-based accounting software. All communication, document sharing, and reporting happens online no physical meetings required.

In practical terms, a virtual bookkeeper does exactly the same work as an in-house or traditional bookkeeper:

Recording all sales and purchases in the accounting system

Reconciling bank accounts and credit card statements

Processing VAT returns and submitting them to Revenue

Running payroll and submitting real-time PAYE reports

Producing monthly management accounts and financial reports

Preparing the books for year-end accounts and tax returns

The difference is that all of this happens remotely, through cloud software that both you and your bookkeeper can access from anywhere. You share documents digitally through a scanning app, email, or an automated feed from your bank and your bookkeeper processes them, keeping your records current and accurate.

For you as a business owner, the experience is that your books are always up to date, your VAT is always filed on time, and you can see your financial position in real time without the overhead of managing an employee or the hassle of physically delivering paperwork to an accountant’s office.

How Virtual Bookkeeping Works in Practice

Understanding the practical mechanics of virtual bookkeeping removes the uncertainty that keeps some business owners from making the switch.

Step 1: Onboarding Your virtual bookkeeping provider reviews your current records and sets up your cloud accounting software or connects to the system you already use. If you are switching from paper-based or desktop bookkeeping, they will manage the migration of your historical data.

Step 2: Document Collection You share your financial documents invoices, receipts, bank statements, supplier bills through an agreed channel. Most businesses use a combination of automated bank feeds (which pull transactions directly from your bank into the accounting software), a document scanning app like Dext on your phone, and email for specific documents.

Step 3: Processing and Reconciliation Your bookkeeper processes all transactions, categorises income and expenditure, reconciles your bank accounts, and ensures your records match your actual bank position. This happens continuously weekly or monthly depending on your transaction volume.

Step 4: VAT and Payroll Compliance At the appropriate intervals typically every two months for VAT and every pay period for payroll your bookkeeper prepares and submits your VAT3 return to Revenue and processes your payroll under the PAYE Modernisation real-time reporting system.

Step 5: Reporting At the end of each month, you receive management accounts a profit and loss statement, balance sheet, and cash flow report giving you a clear picture of your business’s financial position.

Step 6: Year-End Handover At your financial year end, your virtual bookkeeper prepares a clean, fully reconciled trial balance and passes it to your accountant for statutory financial statements and tax returns. Because the books are well-maintained throughout the year, this process is fast and straightforward.

Irish Revenue Compliance and Virtual Bookkeeping

This is where Irish businesses need to be particularly careful. Virtual bookkeeping providers based outside Ireland or generic cloud accounting platforms without Irish-specific expertise may not be familiar with the specific compliance requirements of the Irish tax system.

Here is what Irish Revenue compliance looks like for a typical Irish limited company, and how virtual bookkeeping covers each obligation:

VAT Value Added Tax: Irish VAT-registered businesses must file a VAT3 return with Revenue every two months (bi-monthly). The standard VAT rate is 23%, with reduced rates of 13.5% and 9% applying to specific goods and services. Your virtual bookkeeper calculates your VAT liability or refund position, prepares the VAT3, and files it through Revenue Online Service (ROS) before the deadline.

For businesses involved in EU cross-border trade, Intrastat and VIES reporting obligations also apply. For e-commerce businesses selling to EU consumers, the One Stop Shop (OSS) VAT scheme requires separate reporting. A competent Irish virtual bookkeeper will manage all of these.

PAYE Modernisation Real-Time Payroll Reporting: Since January 2019, all Irish employers are required to submit payroll data to Revenue in real time a payroll submission must be made on or before the date each employee is paid. This is called PAYE Modernisation (or PMOD). Your virtual bookkeeper runs your payroll through compliant software and submits the required Payroll Submission Request (PSR) to Revenue for every payroll run.

RCT Relevant Contracts Tax: RCT is a withholding tax mechanism that applies specifically to payments made by principal contractors to subcontractors in the construction, forestry, and meat processing sectors. If your business operates in any of these sectors and uses subcontractors, you have specific obligations:

You must notify Revenue of each contract before work begins (Contract Notification)

You must notify Revenue before making each payment (Payment Notification)

Revenue then issues a deduction authorisation specifying whether 0%, 20%, or 35% should be withheld

You must submit an RCT Return (Form RCT30) monthly

RCT is an area where many businesses make compliance errors because the obligations are triggered at payment stage not at month end. A virtual bookkeeper with RCT experience will manage each payment notification in real time, ensuring you never make a payment without the required authorisation.

Corporation Tax: Irish companies pay corporation tax at 12.5% on trading profits. The corporation tax return (Form CT1) must be filed with Revenue within nine months of the company’s financial year end. Preliminary tax must be paid during the year. Your virtual bookkeeper maintains the records that form the basis of your corporation tax return the actual return is typically prepared by your accountant, working from the clean trial balance your bookkeeper provides.

CRO Annual Return: Every Irish company must file an annual return with the Companies Registration Office (CRO) under the Companies Act 2014. Financial statements (profit and loss account and balance sheet) must be attached to the annual return for most companies. Your virtual bookkeeper’s records form the basis of these financial statements well-maintained books make the annual return preparation significantly faster and less expensive.

Cloud Accounting Software Used for Virtual Bookkeeping in Ireland

The technology infrastructure of virtual bookkeeping is cloud accounting software. Here is a practical overview of the most widely used platforms in Ireland.

Xero: Xero is the most widely adopted cloud accounting platform among Irish SMEs and professional bookkeepers. It offers automated bank feeds, strong invoicing tools, multi-currency support, payroll integration, and a large ecosystem of add-on applications. It connects seamlessly with document capture tools like Dext and Hubdoc, which automate the extraction of data from receipts and supplier invoices.

Xero is particularly strong for businesses with inventory, multi-currency transactions, or complex reporting needs. Its real-time dashboard gives business owners an immediate view of cash position, outstanding invoices, and upcoming payments.

QuickBooks Online: QuickBooks Online is a close competitor to Xero and is widely used by Irish sole traders, contractors, and SMEs. It has strong payroll integration, good VAT handling for Irish tax rates, and a straightforward interface that many business owners find easy to use directly.

Sage Business Cloud: Sage has a long history in Irish accounting and its cloud version maintains a strong user base particularly among retail businesses, larger SMEs, and companies with existing Sage desktop installations transitioning to cloud. Sage has strong Irish VAT support and integrates well with EPOS (electronic point of sale) systems.

FreeAgent: FreeAgent is particularly popular with contractors, freelancers, and sole traders. It has built-in invoicing, expense tracking, VAT return preparation, and Self Assessment (income tax) support. Its interface is designed for non-accountants, making it accessible for business owners who want to stay involved in their own bookkeeping.

Dext (formerly Receipt Bank): Dext is not a full accounting system it is a document capture and automated data extraction tool that sits alongside Xero, QuickBooks, or Sage. Business owners photograph receipts and supplier invoices using the Dext mobile app. Dext reads the data supplier name, amount, VAT and pushes it automatically into the accounting system, eliminating manual data entry. For high-volume receipt businesses, this is a significant time saver.

Hubdoc: Hubdoc serves a similar purpose to Dext, with particularly strong capability in automatically fetching supplier statements, utility bills, and bank statements directly from online portals. It is included free with Xero subscriptions.

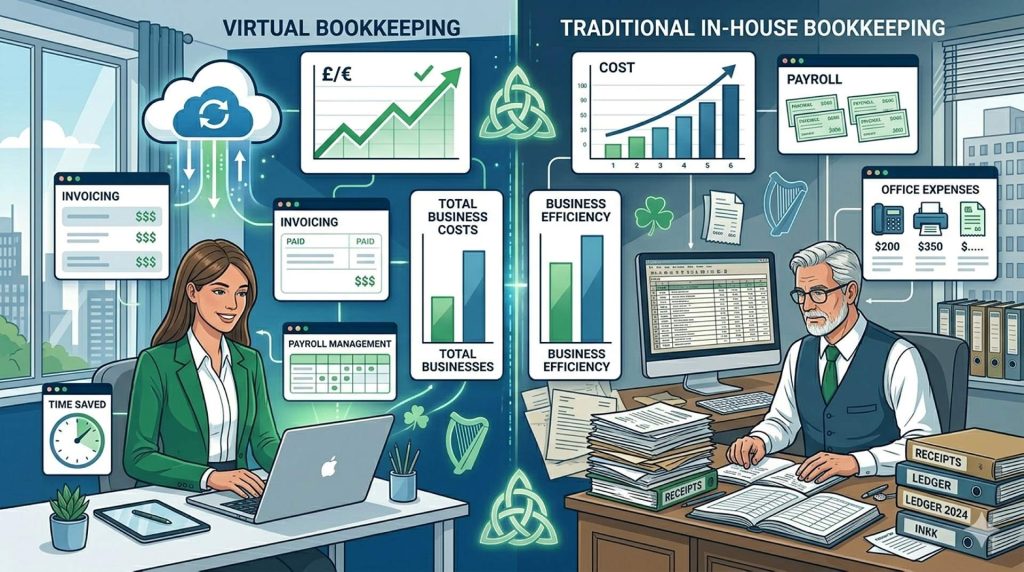

The Real Cost of Virtual Bookkeeping vs In-House

Cost is one of the first questions Irish business owners ask about virtual bookkeeping. The comparison with in-house bookkeeping is almost always favourable but it is worth understanding why.

The true cost of an in-house bookkeeper in Ireland

The advertised salary is only part of the cost. A bookkeeper earning €35,000 per year costs significantly more to employ:

Gross salary: €35,000

Employer PRSI (11.15%): ~€3,900

Annual leave cover: 20+ days per year

Sick leave: statutory entitlements plus potential for longer absences

Training and software: CPD, software licences

Recruitment cost: typically one to two months’ salary for a replacement

Total real annual cost: typically €40,000–€50,000 for a bookkeeper at this salary level before accounting for gaps in cover during holidays and illness.

The cost of virtual bookkeeping

Virtual bookkeeping is typically priced as a fixed monthly fee based on transaction volume and the specific services required. For a straightforward SME monthly bank reconciliation, bi-monthly VAT returns, monthly payroll for a small team, and monthly management accounts monthly fees from a quality Irish provider typically range significantly below the equivalent in-house cost.

Beyond the direct cost saving, virtual bookkeeping eliminates:

Technology cost software licences are typically included in or managed alongside the service fee

Recruitment risk finding, hiring, and replacing bookkeeping staff

Knowledge risk the risk of a sole in-house bookkeeper leaving and taking institutional knowledge with them

Coverage risk no impact on your books when someone is sick or on leave

What Virtual Bookkeeping Cannot Do

No guide on this topic should overstate what virtual bookkeeping delivers. There are specific things it is not designed to handle, and understanding the boundaries helps you make the right decision.

Virtual bookkeeping is not tax planning: A bookkeeper records and reconciles transactions they do not advise on tax strategy, profit extraction, pension contributions, capital gains planning, or inheritance tax. For tax planning advice, you need a tax consultant. TAS Consulting provides both services, which means your bookkeeping and your tax planning are always aligned.

Virtual bookkeeping is not financial advisory: Your virtual bookkeeper produces management accounts and reports they do not provide investment advice, business valuation, or corporate finance services.

Virtual bookkeeping is not auditing: If your company is required to have its financial statements audited under the Companies Act 2014, that is a separate engagement with a registered auditor. Your virtual bookkeeper’s records form the basis of the audit they do not conduct it.

Understanding these distinctions helps you build the right team of professional advisors around your business.

How to Switch to Virtual Bookkeeping Without Disrupting Your Business

The most common concern business owners express about switching to virtual bookkeeping is continuity what happens to their existing records, and how long will it take to get the new system running properly?

Here is a realistic guide to a smooth transition.

Choose your switch point carefully: The start of a new financial year or a new VAT period is the cleanest point to switch. This avoids mid-period complications and makes the reconciliation of opening balances straightforward.

Gather your existing records: Before onboarding, your new provider needs to understand where you are starting from your latest bank statements, your most recent VAT return, your current payroll position, and any outstanding debtors or creditors. The more organised your existing records, the faster the setup.

Agree on document sharing: Decide how you will send documents phone app, email, or automated bank feeds. Most virtual bookkeepers will walk you through the setup of automated feeds from your bank, which eliminate the most time-consuming part of document sharing going forward.

Expect a settling-in period: The first one to two months of a new virtual bookkeeping relationship typically involve some back-and-forth as your bookkeeper learns your business, your suppliers, and your typical transaction patterns. This is normal and should not be confused with an ongoing problem. By month three, most clients report that the process is almost entirely automatic from their perspective.

Communicate changes promptly: If you take on a new employee, change banks, start selling in a new EU country, or take on a subcontractor, tell your bookkeeper immediately. These changes affect payroll, VAT, and potentially RCT obligations and they need to be reflected in your records from the point the change occurs.

How to Choose the Right Virtual Bookkeeping Provider in Ireland

The quality of virtual bookkeeping providers in Ireland varies significantly. Here is what to look for before you engage anyone.

Irish-based and Revenue-literate: Your provider must understand Irish tax law specifically Irish VAT rates and rules, PAYE Modernisation, RCT, and CRO compliance. International platforms and non-Irish providers frequently miss Irish-specific requirements.

Qualified and professional: Look for providers whose bookkeepers hold relevant qualifications Accounting Technicians Ireland (ATI), Association of Chartered Certified Accountants (ACCA), or equivalent. Unqualified bookkeepers can maintain records, but they lack the technical grounding to handle complex transactions correctly.

Clear, fixed pricing: Your provider should be able to give you a fixed monthly fee based on your transaction volume and service requirements. Be cautious of hourly billing for routine bookkeeping it makes costs unpredictable and incentivises inefficiency.

A full-service firm: A virtual bookkeeping provider that also offers accounting, tax, payroll, and company secretarial services is more valuable than a standalone bookkeeping-only provider. As your business grows, your needs will expand and having a single trusted firm that handles everything is significantly more efficient.

Responsive and proactive: Your provider should contact you about approaching deadlines, flag any Revenue correspondence immediately, and alert you to any unusual patterns in your financial data. The best virtual bookkeepers are proactive they tell you what you need to know before you think to ask.

Clear data security protocols: Ask specifically how your financial data is stored, who has access, and what happens to your data if you end the engagement. All reputable providers use encrypted, SOC-2 compliant cloud platforms.

Start Your Business Journey Now

Hundreds of startups already growing with TAS Consulting

Your Business Deserves Books That Are Always Up to Date

TAS Consulting’s virtual bookkeeping service gives Irish businesses professional, fully compliant bookkeeping remotely managed, cloud-based, and built around your Revenue obligations. Get in touch today for a free consultation and a transparent quote.

Frequently Asked Questions

What is the difference between a bookkeeper and an accountant in Ireland?

A bookkeeper records and maintains daily financial transactions invoices, receipts, bank reconciliations, payroll, and VAT returns. An accountant uses those records to prepare statutory financial statements, corporation tax returns, and strategic tax advice. In Ireland, both roles are required for a fully compliant limited company. Virtual bookkeeping handles the bookkeeping layer your accountant uses the output for year-end compliance.

Do I need to be VAT-registered to use a virtual bookkeeping service?

No. Virtual bookkeeping is available to all businesses VAT-registered and non-VAT-registered. If your turnover is below the Irish VAT registration threshold (€80,000 for goods, €40,000 for services in 2026), you may not yet be required to register. Your virtual bookkeeper will monitor your turnover and advise when registration is approaching.

Is cloud accounting data safe?

Yes, when you use reputable platforms. Xero, QuickBooks, Sage, and FreeAgent all use bank-grade encryption, two-factor authentication, and regular third-party security audits. Your financial data in a cloud accounting system is significantly more secure than on a local desktop computer or in a physical filing system.

Can a virtual bookkeeper represent me in a Revenue audit?

Your virtual bookkeeper can support you through a Revenue audit by providing access to all underlying records, preparing reconciliations, and explaining specific transactions. Formal representation in Revenue audit proceedings particularly in a formal investigation requires a qualified tax agent or solicitor. TAS Consulting provides both bookkeeping and tax advisory services, meaning we can support you through the full audit process.